My most recent article argued that there is a missing market between the two major exchange markets, spot and futures, and missing instruments that link the present to the future. In an earlier article, I described the instruments that might be traded in the missing market, two exchange-traded index instruments. That article describes how to create an exchange-traded interest rate swap.

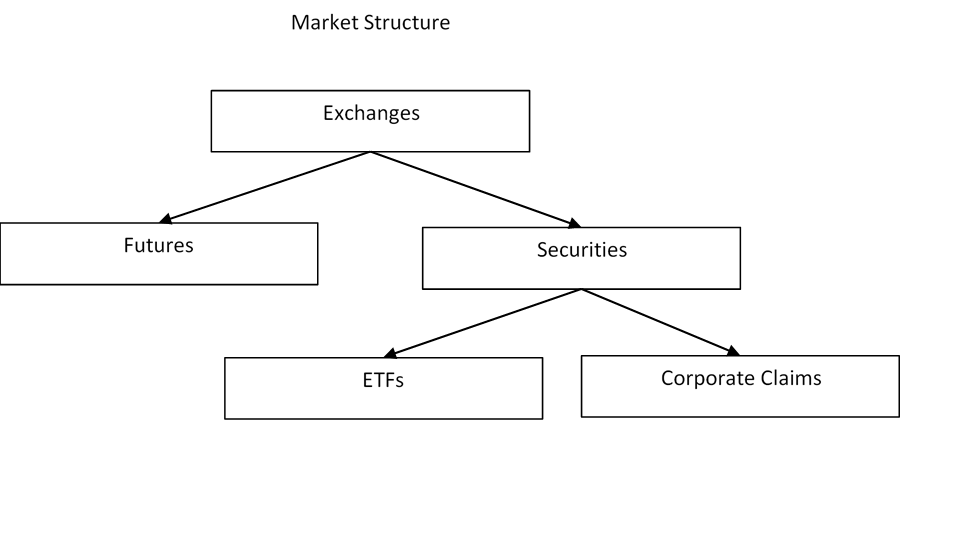

The current state of the market structure is described in the Market Structure graphic below. The graphic shows that securities exchanges appear in two forms – securities markets and index spot markets (ETFs). Futures markets, however, have no second form.

Source: Author, Market Structure graphic

The article made the case for adding a hybrid market, intermediate between spot and futures markets. This new hybrid market would trade exchange originated instruments (EOIs) that are traded like futures but settle by delivery of a spot instrument originated by the listing exchange.

In comparison to futures markets, this both-spot-and-futures exchange would have a critical advantage – the control of the futures contract’s associated spot market. The added capability would prevent the type of disaster looming over the CME Group (CME). CME is in danger of losing its biggest ticket, Eurodollar futures, because LIBOR, Eurodollars’ associated spot market, is dying. The underlying weakness that the Eurodollar market exemplifies is pervasive in futures-only markets. Futures markets lack control of their related spot markets.

Perhaps the greatest advantage EOIs provide to a securities or futures exchange is that both spot and futures are in sole exchange control. The advantages are many:

- The risk from the exchange point of view is less.

- The risk from a market participant’s point of view is less.

- Transactions cost is minimized.

- Alternatives from the point of view of the market are maximized.

- Market regulators maximize their ability to monitor the performance of the market.

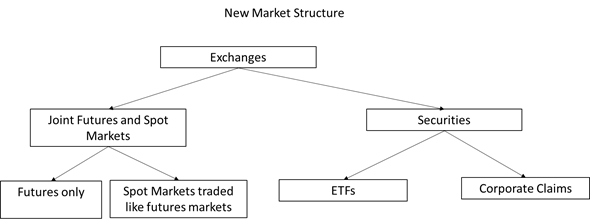

The “New Market Structure” graphic below displays the location of the market within the broader structure of exchanges generally. The market could be described either as a spot market for indexes traded like futures contracts or as a financial futures market with self-settling futures contracts.

Source: Author, New Market Structure graphic

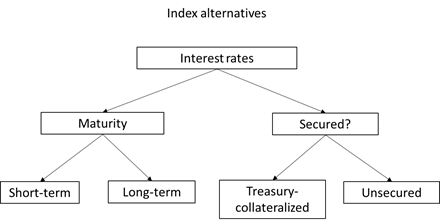

In the second article, I described a way to create two exchange-traded index instruments – secured Treasury-like indexes, and commercial paper-like indexes. What do they do, why do we need them, and how will they perform their function? In a nutshell, the two new indexes augment the Secured Overnight Financing Rate (SOFR), the current regulator-supported LIBOR replacement index. Here are the functions, reasons, and means.

- Purpose: Provide a hedge against collateralized and uncollateralized market risk.

- Motive: SOFR is not function-appropriate.

- Means:…