EURUSD, EURJPY, Dollar, S&P 500 and Ethereum Talking Points:

- The past week ended with further favorable news between US spending and the Amazon earnings aftermath, but yet again, risk appetite refused to take hold

- The S&P 500 closed out its most restrained week’s range since the Christmas holiday of 2019

- A sharp Dollar rebound (EURUSD tumble) may just be short-term seasonality adjustment or perhaps a sign of trends to play out over the week ahead

Risk Trends Refuse to Budget When All Green Lights, But Something Will Rouse Markets

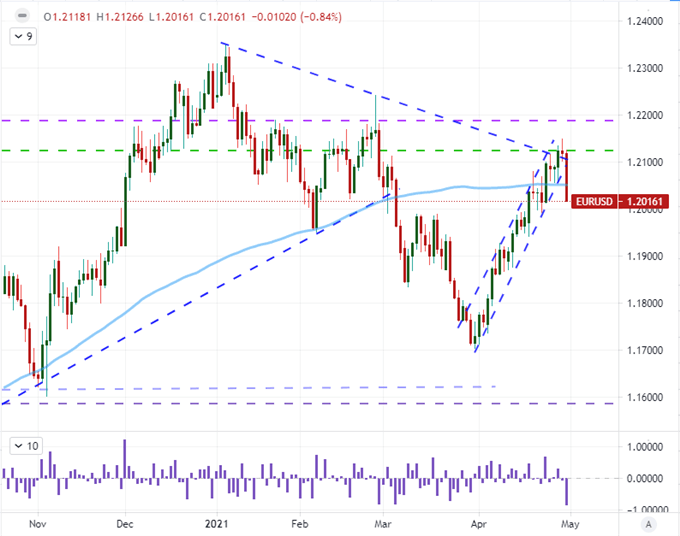

The incredible lack of traction from risk-leaning markets was impossible to miss this past week. Despite a run of typically high-profile, market-moving event risk from Fed dovishness to Presidential stimulus hawking to impressive tech earnings results to the fastest pace of US growth in decades, the benchmarks of ‘risk appetite’ refused to extend the already mature bullish trend of the past year (and decade). This wasn’t just an abstract obliviousness from a further unrelated asset like carry, it was also the US indices which were well within the blast radius of the data. For those that revert to the ‘traditional fundamentals are broken’ line, this has happened many times before and influence has waxed and waned. Perhaps that return of influence is already close at hand with EURUSD signaling a reversal of focus. Itself prone to complacency and following inertia, the pair put in for its single-largest daily slide since April 2nd, 2020 following a month-long contained bull trend. Of course, the key question for traders is whether this shift in activity and bearing for the pair and broader capital markets will carry over to the new trading week and month.

Chart of EURUSD with 100-Day Moving Average and 1-Day Rate of Change (Daily)

Chart Created on Tradingview Platform

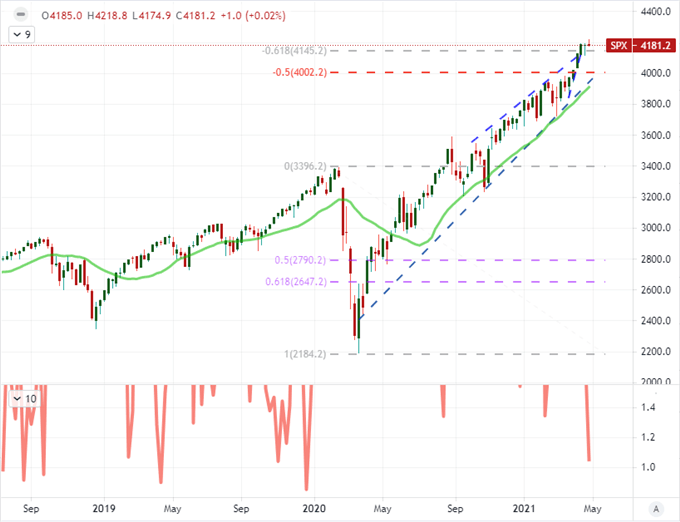

To reiterate just how extraordinary the conditions were that paint the backdrop for the new trading week, I have to once again highlight the S&P 500’s extraordinary inactivity. At the end of the day (week and month), the benchmark index posted its smallest range through the entire week – as a percentage of spot – since the week of Christmas 2019. These should not be comparable conditions. That is especially true given the prevailing trend is clearly bullish and all of the high profile event risk of the past week was tapping the key themes that most often impress the default bullish crowd in the open market. And, just to ensure we don’t misconstrue this as a single benchmarks’ peculiar issue, all the major US indices including the Nasdaq 100 backed by tech earnings suffered the same while alternative risk assets (global indices, emerging market assets, carry trade, junk bonds and more) suffered the same.

Chart of S&P 500 with 20-Week Mov Avg and 1-Week ATR (Weekly)

Read More: EURUSD Posts Biggest Daily Drop in a Year