Global markets were quite choppy this past week. This could follow signs of deteriorating risk appetite judging by recent performance of highly speculative assets. Bitcoin and Ethereum, for example, plunged deeper into bear market territory due to investors fleeing major cryptocurrencies en masse. Equities have been fighting headwinds as well with major stock indices struggling to maintain upward momentum. The Dow Jones closed -0.5% lower on the week, though the DAX managed to gain 0.1% after being down as much as -3.0%.

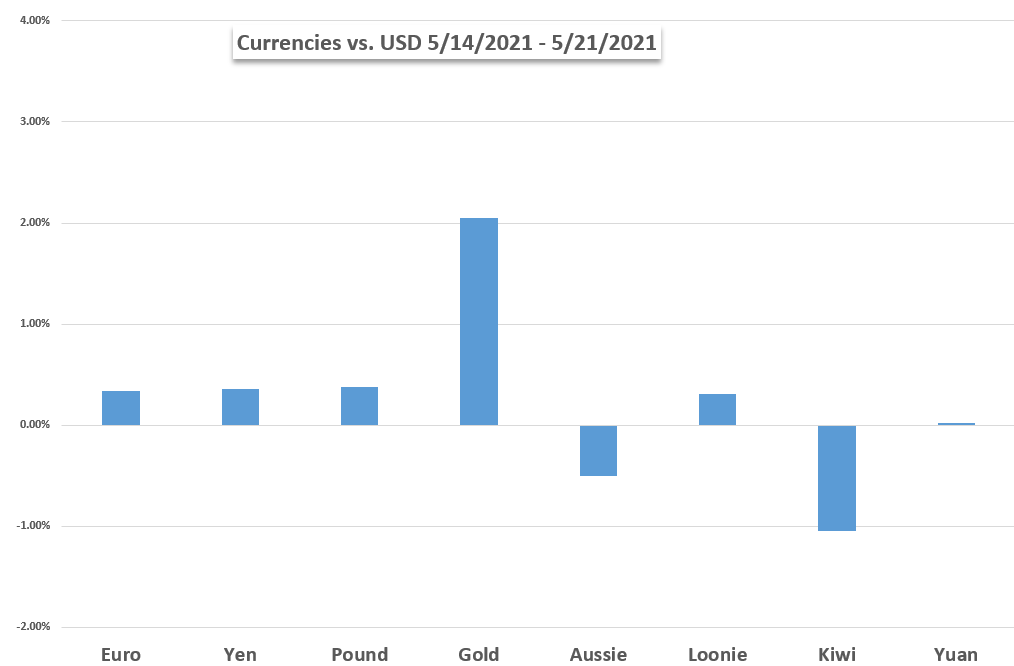

Crude oil prices faced notable selling pressure as commodity traders sank WTI -2.5% and Brent -3.1%. In addition to market sentiment softening broadly, this may be a reflection of traders betting on a potential Iran nuclear deal and spike in global oil supply that would likely follow. Shifting focus to other major commodities, we find that the price of gold extended 2.1% higher to trade around $1,875/oz. This brings the precious metal’s streak of gains to three-weeks straight.

Furthermore, US Treasury bonds saw some demand and pushed ten-year yields slightly lower despite FOMC minutes alluding to the threat of future Fed tapering. The dip in Treasury yields likely weighed negatively on USD price action. Across the board of major currency pairs, US Dollar weakness was felt primarily against the Swiss Franc, Euro, and Yen, but strength was seen relative to the Aussie and Kiwi. EUR/USD advanced 36-pips on the week while USD/CHF, USD/JPY, AUD/USD and NZD/USD declined by 35-pips, 42-pips, 54-pips, and 84-pips, respectively.

US DOLLAR WEEKLY PERFORMANCE AGAINST MAJOR CURRENCIES AND GOLD

Looking to the DailyFX Economic Calendar, we can see that event risk is pretty sparse for the week ahead. There are a few noteworthy items, though. A handful of FOMC officials – like Lael Brainard, Raphael Bostic, and Randal Quarles – are on deck to give remarks and could touch on their thoughts about inflation. Other key central bankers, such as the BoJ’s Kuroda, BoE’s Tenreyro, and ECB’s Guindos, will be giving speeches too. Not to mention, the Reserve Bank of New Zealand is due to announce its latest interest rate decision with RBNZ Governor Adrian Orr expected to provide some additional color on monetary policy guidance during his follow-up press conference.

The release of consumer confidence data could be worth watching out for with the reports potentially swaying domestic market sentiment. Traders might want to keep tabs on infrastructure spending headlines as well after the Biden administration suggested a $1.7-trillion counterproposal to the original $2.3-trillion package. Republicans argued that the latest offer is still ‘too high’ of a price tag. That said, core PCE inflation data out of the US looks like the big-ticket item scheduled to cross market wires Friday, 28 May at 12:30 GMT. What else is in store for markets during…

Read More: EUR/USD, Gold, Oil, Bitcoin, Dow, DAX, Inflation, RBNZ