Fundamental Forecast for the US Dollar: Neutral

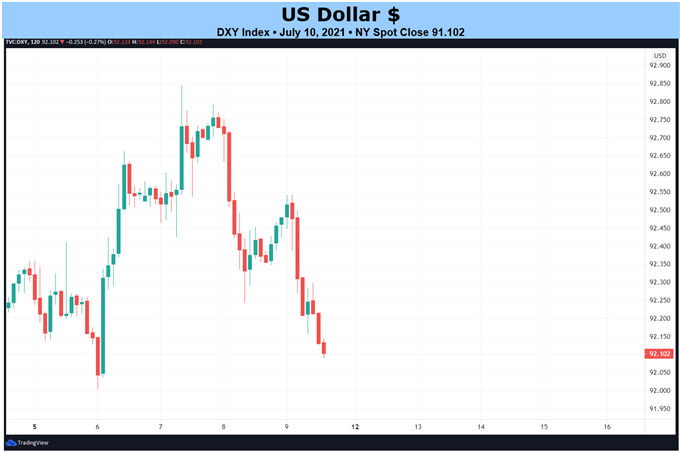

- The US Dollar (via the DXY Index) has dropped back as the calendar moved into mid-July on the back of declining Fed rate hike expectations and collapsing US Treasury yields.

- And even though another hot inflation report is anticipated, markets are actually becoming less convinced that the Fed will hike interest rates anytime soon; action will be constrained to tapering off asset purchases.

- According to the IG Client Sentiment Index, the US Dollar has a mixed bias heading through the middle of July.

US Dollar Back Down

The US Dollar (via the DXY Index) has dropped back as the calendar moved into mid-July on the back of declining Fed rate hike expectations and collapsing US Treasury yields. But with a potent catalyst due over the coming days – the June US inflation (CPI) report on Tuesday – a shift in the recent narrative may be around the corner.

While hot inflation readings should theoretically spill into higher US Treasury yields, the fact that the Federal Reserve continues to resolutely insist that inflation is “largely transitory” may prevent significant topside move in yields. Accordingly, there is asymmetric risk for the US Dollar: a hot inflation report may not do anything to push yields higher; a softer inflation reading could justify another leg lower in yields.

US Economic Calendar Loaded with Risk

The move into the middle of the month brings forth a meaningful docket of event risk based out of the US. Several high rated economic releases coupled with Fed Chair Jerome Powell’s semi-annual Congressional testimony make for a potentially

- On Tuesday, July 13, the June US inflation report (CPI) will be released, with elevated inflation rates expected to persist. Also on Tuesday, the US federal government’s monthly budget statement for June is set for publication.

- On Wednesday, July 14, a separate June US inflation report (PPI) will be released, looking at input costs for businesses (e.g. ‘at the factory gate’). Fed Chair Powell will head to Capitol Hill for day 1 of 2 of his Congressional testimony, reflecting on the contents of the July Monetary Policy Report that was released on July 9. Later in the day, the Fed’s Beige Book will be released.

- On Thursday, July 15, the weekly jobless claims data is due ahead of the July Philadelphia Fed manufacturing index. Later, June US industrial production figures will be released. Finally, Fed Chair Powell will return to Capitol Hill for day 2 of 2 of his Congressional testimony.

- On Friday, July 16, the June US retail sales report was released before the preliminary July US Michigan consumer sentiment report, including 5-year inflation expectations. At the end of the day, the US Treasury’s foreign bond investment report and overall net capital flows data for May will be released.

Atlanta Fed GDPNow 2Q’21 Growth Estimate (July 9, 2021) (Chart…

Read More: Will Hot Inflation Spark US Yields Again?