Markets swung wildly last week as fears over the delta variant of covid bulged then faded. This initially caused a notable deterioration in risk appetite that steered stocks sharply lower. The Dow Jones, Nasdaq, and S&P 500 were down between -1.5% and -2.7% at their low points, but as sentiment recovered amid prevailing ‘buy-the-dip’ mentality, these major stock indices ended up finishing the week at record highs yet again.

Bonds behaved similarly with economic growth concerns initially sending Treasury yields on a steep descent that reversed as trading progressed. Likewise, crude oil prices dropped as much as -8.7% last week only to erase those losses and finish 0.7% higher on balance. This wave of volatility briefly fueled huge spikes in the VIX Index and OVX Index to hit nine-week and 13-month highs, respectively. The VIX Index and OVX Index closed lower on the week nevertheless as market angst subsided.

Although, the MOVE Index, which is a 30-day implied volatility reading derived from options on Treasury bonds, finished the week at its highest level since March. To that end, with bond market volatility expected to stay elevated, there is potential for other asset classes like stocks, commodities, and currencies to continue experiencing violent gyrations alongside yields. This seems quite reasonable – particularly when considering the plethora of high-impact risk events and data releases scheduled on the economic calendar for the week ahead.

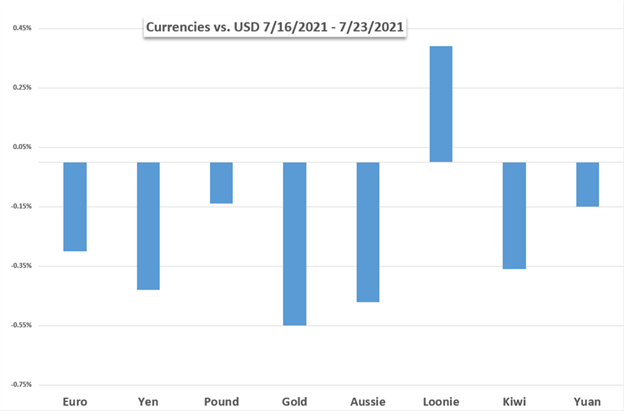

MAJOR CURRENCIES AND GOLD PERFORMANCE AGAINST US DOLLAR

The Federal Reserve meeting on deck arguably stands out as the biggest catalyst for volatility due to its often market-moving potential. While the Fed announcement due Wednesday, 28 July at 18:00 GMT is widely expected to leave monetary policy unchanged, there is growing risk that the central bank tweaks language to its press statement. As such, traders will likely have a keen eye out for guidance on the FOMC’s substantial further progress objective and potential upcoming adjustments to the pace of asset purchases.

This brings US Dollar price action into focus as a barometer for gauging the market’s relative hawkish or dovish read on the Fed. US Dollar strength across the board of major currency pairs next week might indicate that the Fed is taking inflation and taper talks seriously. On the other hand, a weaker US Dollar post-Fed could indicate that the central bank is sticking to its transitory inflation narrative and staying cautiously accommodative. The latter scenario would likely correspond with positive boosts to risk assets and precious metals like gold and silver.

Traders will be watching for updated inflation data out of the US, Eurozone, Canada, and Australia on tap next week as well. Progress reports on economic recoveries across the US and Euro-area will also be provided with advanced Q2 GDP data slated for release. The Euro,…

Read More: Euro, Dollar, Gold, S&P 500, Fed, Earnings, Inflation