A traffic light is seen near the headquarters of China Evergrande Group in Shenzhen, Guangdong province, China September 26, 2021. REUTERS/Aly Song/File Photo

SHANGHAI/LONDON, Oct 21 (Reuters) – Numbers don’t lie, you just need to be looking at the right ones.

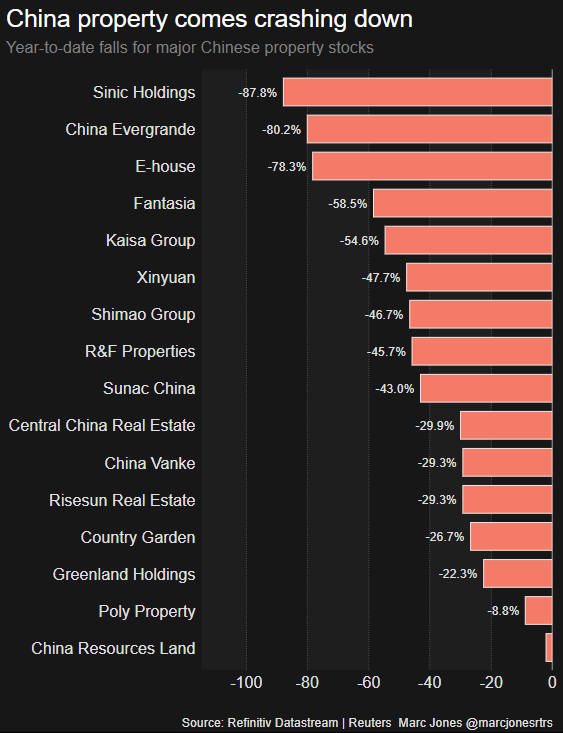

That’s the problem for investors searching for the next trouble spot in the Chinese real estate sector as industry giant China Evergrande Group (3333.HK)lumbers towards what is expected to be the country’s largest-ever corporate default. The figures on the books sometimes don’t tell the full story.

Since Beijing started clamping down on corporate debt in 2017, many real estate developers have turned to off-balance-sheet vehicles to borrow money and skirt regulatory scrutiny, analysts and lawyers say.

Joint ventures are a popular choice because, unless a company holds a controlling interest in one, it can keep details of it and the debt it acquires off its balance sheet.

“Nearly every developer has borrowings in disguise. The sector’s debt problem is worse than what you see,” said He Siwei, attorney at Hui Ye Law Firm.

Chinese developers owed 33.5 trillion yuan ($5.24 trillion)through various channels at the end of June, Nomura estimates, based on official statistics, adding “there are definitely other obscure financing channels yet to be covered.”

Private bonds issued by shell companies in offshore locations have emerged as a new concern.

In a note this month, Fitch ratings agency said that Fantasia Holdings Group (1777.HK), a property developer which has since defaulted, had recently told it “for the first time” that it had $150 million of private bonds that do not appear to have been reported in its financial statements.

Fantasia did not respond to a request for comment. The company had over $4 billion worth of cash at the end of June and two weeks before it defaulted said that it had “ample capital”.

Unsurprisingly, investors have begun to look in less obvious places as the sectors’ most troubled firms have been locked out of international capital markets.

Some of those developers hit hardest had better-looking financials than those whose bonds had been less impacted, according to an analysis by JPMorgan, underlining a lack of faith in balance sheets.

Out of 70 Chinese property developers rated by Moody’s, 27 have “significant” exposure to joint ventures, compared with five out of 49 in 2015.

Under a typical joint venture, a developer sets up a minority-owned real estate project with an asset manager or private equity fund and promises them fixed returns. The developer usually agrees to buy back its stake from the other investor after a certain number of years.

Read More: Analysis: What lies beneath? Hidden debt fears feed China’s property woes